ABC Equity Portfolio - Apr '24 update

Investing in transformational trends core to India's transition from a low income to a middle income economy

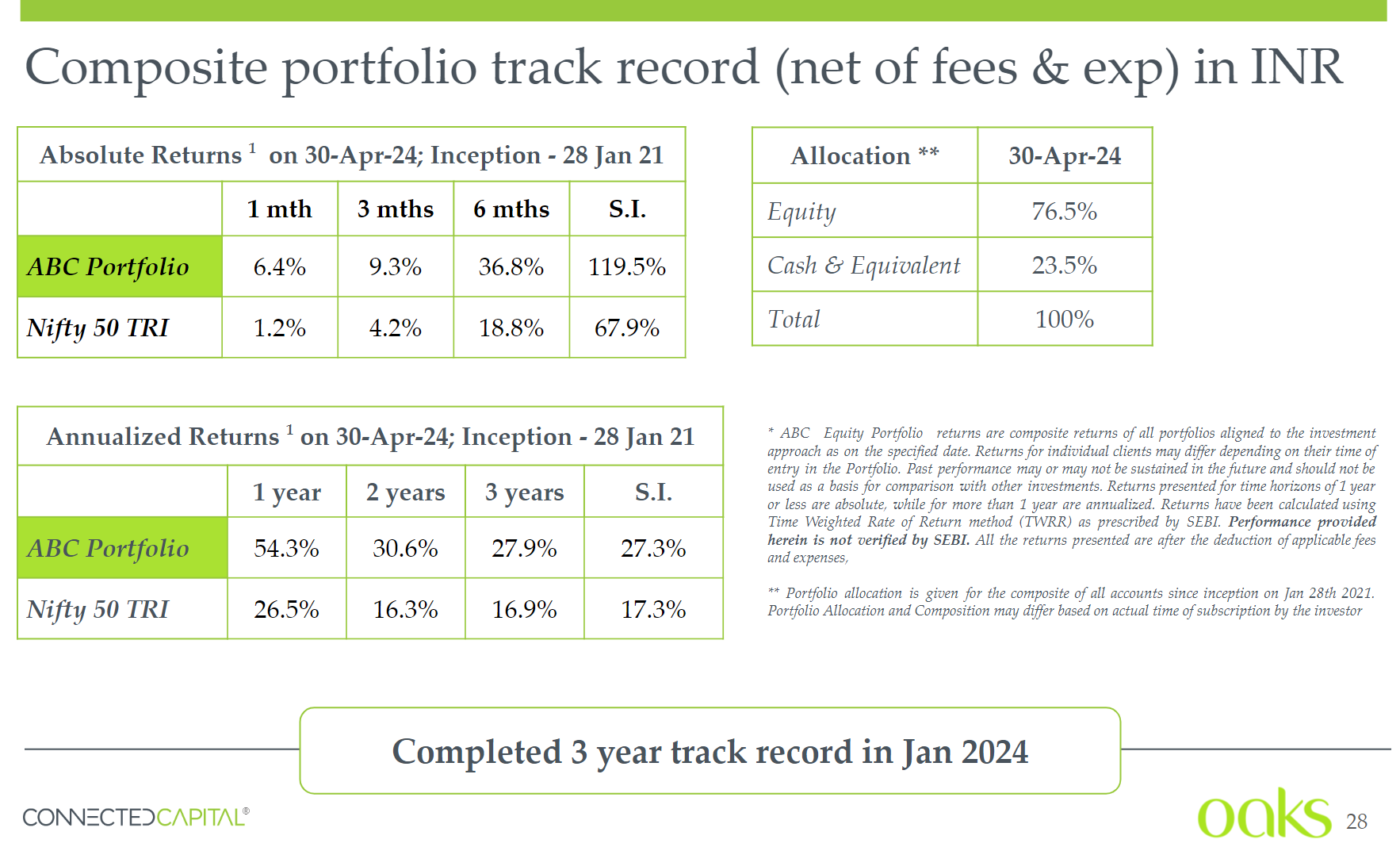

Performance

Apr’24 saw weakness across most major equity markets with the exception of the two laggards of 2023 i.e. Chinese H-shares & UK along with India bucking the downtrend. Currencies and Bonds ended flat masking sharp intra-month volatility with the JPY falling steeply prior to a BoJ intervention (See below). Bitcoin, Gold, Agri-commodities and Oil saw a corrective break of their strong 2024 rallies, while industrial metals continued to move up.

Indian equity markets were strong in April especially in the small cap, midcap and smaller large cap categories with the respective indices hitting new highs and significantly outperforming the Nifty 50. Net sales of INR 35k cr (~4.3 bln$) by Foreign institutions (FPI) was more than matched by INR 44k cr (5.3 bln$) of net buying by domestic institutions (DII) continuing the pattern seen in CY24. Sectoral returns showed considerable divergence with Metals & State owned firms being the best while IT and pharma were weakest. The INR and Indian bond yields largely mirrored global trends.

Developments in trends we invest into in the ABC Portfolio

Manufacturing ecosystem – We capture this via input providers like energy, materials & automation. Energy transition initiatives saw bids for EV battery manufacturing, setting up green hydrogen & green ammonia plants at Kandla port and allowing FPIs to invest in Sovereign Green Bonds. Developing the critical mineral supply chain from sourcing to processing is another priority with work underway for global partnerships in processing technology.

Organized agri-business – We capture this via the farm to fork supply chain & fertilizers. Discussions have been on regarding the crucial role of agriculture in India’s developmental path, with emphasis on addressing the trust deficit between governments & farmers, scientific agricultural practices, mitigating impact of climate disruptions and income support policies.

Supporting infrastructure – We capture this via infrastructure, logistics and real estate. Infrastructure projects are the cornerstone of the BJP’s manifesto, so activity is likely to be galvanized should they come back in power. The focus of the infrastructure and logistics buildout is to transform India into a global manufacturing base.

National Champions – We capture this by replicating the Chinese strategy of consolidating the state owned banking and oil & gas sectors, and developing the life insurance sector. To expand the insurance coverage of the population, a three pronged strategy across simplified bundled plans, online portals and offline distribution is being planned.

Digital platforms – We capture this via firms which use India’s digital public goods initiative as the foundation to offer products & services. The RBI brought out a draft guideline on digital lending, where the lending service provider will need to display loan offers from all lenders it has tie-ups with.

Summary & Outlook

April saw a sharp rise in US bond yields and the USD-JPY (Yen depreciation) in the build up to the Fed meeting on 1st May. The Bank of Japan intervened a day prior causing the USDJPY to retreat rapidly. This was followed by the FED reducing the amount of balance sheet run-off. The actions by these major central banks (possibly coordinated), effectively reduces the tightening of the global financial system. With bitcoin, gold, stocks and agri-commodities also having corrected this month, it can increase the probability of a resumption in their up move in May.

The large outperformance of the Nifty Next 50, Nifty Midcap 150 and Nifty Smallcap 250 indices v/s the Nifty 50 in CY24 (see below) shows the breadth in Indian equity markets. All 3 indices hit decisive new highs in April, driven by domestic investor flows, as net buying of INR ~155k cr (18.6bln$) by DIIs comfortably absorbed the ~ INR 84k cr (10bln$) selling by FPIs.

A key driver for domestic investors has been the favorable tax treatment of equities v/s fixed income. This condition is unlikely to change till we have the next budget in July from the new government. With global conditions easing and Indian election results due early June, FPI participation may also increase and likely lead to any corrections being bought into.

At the same time, stocks are at higher valuations v/s historical averages and the current rally has lasted over 12 months with only minor corrections. This leaves little margin for error in case there are any expectation mismatches or untoward incident out of left field.

Given this duality, we maintained our stance of participating in the rally by allocating to sectors that match the strategic focus of the government, while keeping a large cash buffer to use opportunistically during corrections.