ABC Portfolio - Apr '23 update

Performance & Portfolio updates - Apr '23

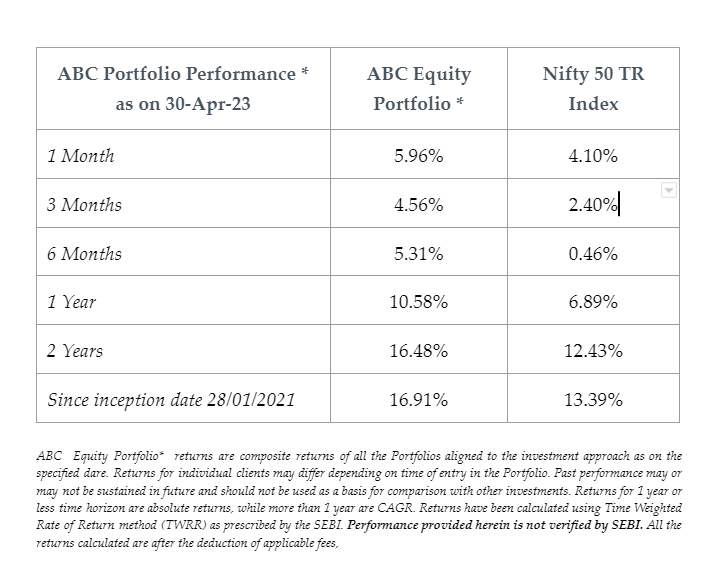

Performance

April ’23 was a period of relative calm across global markets post the volatility seen in March ‘23. Global bond and currency markets were stable and most equity markets were positive. Commentary around a weakening global economy and approaching US debt ceiling debates kept the US dollar weak, thereby supporting global assets. The narrative on de-dollarization gathered steam, with a perceived challenge emerging from a potential BRICS+ currency.

Indian equity and bond markets outperformed their global counterparts for the first time in CY2023. The small net buying seen by FPI’s in Mar’23 increased marginally in April. Strong markets improved sentiment and one could see increasing buying interest as the markets climbed higher. Realty, PSU banks & Auto were the best performers while IT services was the worst.

Developments in trends we invest into in the ABC Portfolio

Manufacturing ecosystem – We capture this via input providers like energy, materials & automation. The thrust to set up a renewable energy ecosystem across solar, nuclear, wind and green hydrogen can be seen from private and public sector companies. Domestic mining & metal firms are trying to secure raw material supply for e-mobility in mineral rich countries.

Organized agri-business – We capture this via the farm to fork supply chain, plantations & fertilizers. Attempts at building an integrated supply chain can be seen with supply chain start-ups expanding into processed food brands and food companies looking to secure input supplies.

Supporting infrastructure – We capture this via infrastructure, logistics and real estate companies. Activity levels are high especially in building highways, a wide range of railway projects and metro rail networks in multiple cities.

National Champions – We capture this by replicating the Chinese strategy of consolidating the state owned banking and oil & gas sectors. Softer crude oil prices and strong demand is allowing the oil & gas firms to recover some of the losses they had to incur in 2022. The government may also infuse equity in some of these firms to support their capital expenditure plans.

Digital platforms – We capture this sector via digital platforms which can benefit from the implementation of IndiaStack. There has been a flurry of deal activity in the fintech - NBFC space as RBI’s new digital lending norms make it essential for fintech firms to have an NBFC to stay competitive. Our portfolio company in this space is likely to spin off one of the largest digital lending NBFC’s over the next few months.

Summary & Outlook

We scaled up equity allocations in the portfolio from ~85% in late March to ~93% in April. Multiple sectors participated in the rally through April with isolated pockets of euphoria emerging by month-end. This pendulum swing from apathy to enthusiasm is something we will watch closely in May.

- Globally, at the time of writing, more regional banks in the US have gone bankrupt, which will further concentrate power with a few giant banks. This may cause a credit contraction in the next few months and with the debt ceiling debate looming, there maybe heightened volatility in the markets.

- In India, as tax benefits on most fixed income options ended in March, equities will be a natural destination for large pools of domestic capital. Thus one would expect that any corrections will likely be well bid.